In the aftermath of the ICO boom and bust, the decentralized finance community continued to expand financial products and services that are based on digital assets. This continuing expansion and attempts to disrupt existing legacy finance via decentralized finance products gave rise to what became known as Decentralized Finance (DeFi).

The historical evolution of DeFi begins in early 2018. It was then that the teams behind Set Protocol, 0x, Dharma, and DyDx started working together to build an alternative financial system. The teams hoped they would be able to address the fairness, transparency, and equity issues that afflict the existing system.[1] As it evolved, the DeFi movement became an open community for decentralized finance platforms to work toward these goals together to achieve open source interoperability, collaboration, and transparency.[2] Telegram and Reddit channels were subsequently created, followed by meetups and soon conferences called “DeFi Summits”. In the early 2020s, DeFi’s total value had risen to~US$500M.[3] DeFi applications became more robust and the community started launching second-generation protocols. DeFi became the leading sector of the cryptocurrency market.[4] Any FinTech project can become part of the DeFi community if it builds a service for or is based on blockchain, based on general standards and is compatible with other DeFi projects, and fulfills these principles.[5]

The Ethereum platform enabled the evolution of DeFi. Ethereum enables an open financial system with little to no involvement from financial institutions.[6] In the early 2020s, Ethereum is the leading DeFi platform for smart contracting and is used by the overwhelming majority of DeFi protocols.[7] Transactions on the Ethereum blockchain are valid, meaning network participants (“nodes”) verify, validate, and audit transactions before and after they are executed.[8] Such transactions are immutable and no third party can reverse a transaction[9] and verifiable through a smart contract.[10] Ethereum’s network technology can thus eliminate the need for intermediaries in financial transactions and expand transaction possibilities by increasing the scope and efficiency of peer-to-peer transactions through distributed trust and decentralized platforms.[11] Less intermediary involvement reduces transaction cost, broadens financial inclusion, empowers open access, encourages permissionless innovation, and creates new business opportunities.[12]

Evolving DeFi platforms keep increasing the financial products and portfolio of services for network participants. For example, DeFi platforms include prediction markets, distributed corporate governance, and trade finance.[13] Banking services have also employed blockchain technology in order to mitigate credit risk for exporters and importers.[14] DeFi platforms allow users to convert fiat currency into a stable currency, store stable currency in an interest-bearing account, and use future contracts to hedge against financial uncertainty.[15] DeFi platforms go beyond traditional banking and financial services. Parties in the supply chain can view inventory records and effect payments in real-time, and could facilitate a seamless system of lending and repayment using smart contracts.[16]

Despite its impressive gains, the evolution of DeFi platforms depends on higher levels of stability in its products and the market for digital assets overall. The evolution of the DeFi market and its new monetary system depends on the stability of DeFi products and digital assets. Stability and adoption of DeFi is undermined by the instability of most cryptocurrencies.[17]

a) Decentralized Exchanges (“DEXs”) & Protocols

A key feature of the DeFi community is its ability to make decentralized protocols available for the benefit of its users. For example, several DeFi protocols enable decentralized peer-to-peer token exchanges (DEX).[18] In the early 2020s, DEXs include EtherDelta, IDEX, 0x, Kyber Network, Uniswap, Ren, and the Bancor Network. Protocols can serve as liquidity reserves to other protocols[19] and parties can even create custom dark pool DEXs.[20]

DEXs have several key characteristics. DEXs can facilitate “swaps,” where trades are conducted directly against smart contract token reserves and prices are determined using a conversion formula. Or DEXs can be similar to a traditional, centralized exchange. Trades can either be settled “on-chain”, wherein trades are finalized and ownership transferred directly on the blockchain, or off-chain where trades are finalized and ownership transferred in a third-party system.[21] DEX order books can be held in a smart contract directly on the blockchain, or a third party can operate the exchange’s order books. Finally, liquidity can either be pooled in smart contracts directly on the blockchain or off-chain, where multiple third-parties aggregate order books to pool liquidity. The majority of DEXs are swap, settle on-chain, pool liquidity on-chain, and either do not include order books or have off-chain order books. Some protocols have their own token, used for governance, paying fees, determining conversion rate for token swaps (or even give users stake, upon which users can gain a yield from transaction fees). [22] For example, Uniswap, a protocol which has approximately 25,000 ETH and $USD 7.1 million in pooled liquidity, does not have its own token.[23]

b) Lending and Borrowing

Lending and borrowing of digital assets are one of the most common services decentralized DeFi protocols make available to their users. The loan market in the existing centralized financial system is ripe for disruption by DeFi Dapps. The 1.7 billion unbanked in the world have very limited access to the loan market because they typically cannot provide the basic documentation required by centralized banking institutions. This excludes the unbanked entirely from the value creation that would be possible if they had access to loans. DeFi platforms grant the unbanked access to the loan market by disintermediating existing banks. DeFi Dapps connect borrowers and lenders in peer-to-peer networks directly. They allow the unbanked to use digital assets as collateral for loans and require often much less documentation than traditional banking institutions.

Users have a few different options for decentralized lending and borrowing through protocols built on Etherum. The most popular lending platforms include MakerDAO, Compound, and Dharma. MakerDAO is a lending protocol that allows users to post ETH as collateral to borrow against. Users of MakerDAO can open a collateralized debt position to borrow against on MakerDAO by posting ETH.[24] MakerDAO accounts for almost ninety percent of total USD value locked in DeFi projects.[25] As a lending platform, Maker remained resilient even as the price of ETH, the asset it lends against, lost much of its value over the course of 2018. MakerDAO’s token, Dai, remained stable in early October 2019 by keeping pegged to within 2% of 1 USD while other cryptocurrencies experienced major volatility.[26]

Compound is a platform launched in September 2018 that enables decentralized money markets that have dynamic interest rates that float in real-time as market conditions adjust.[27] Compound is a smart-contract system that acts as a credit market and accumulates tokens in a liquidity pool through which users can lend or borrow cryptocurrency.[28] Compound is a money market protocol with floating interest rates based on market conditions.[29] Users supply assets to the protocol and can either earn interest or borrow from the protocol and pay interest, as long as the user’s supply balance remains one and one-half times the user’s borrow balance. Users held over $24,000 worth of assets held as collateral on Compound v1.

Compound released the second generation of their protocol in May 2019[30] that includes granular risk modeling, more asset gateways, and governance improvements.[31] Projects on Compound v2[32] include Zerion,[33] a portfolio monitoring and management tool for open finance, and Opyn[34], a decentralized margin trading platform. Compound stores almost 15% of all Dai, one of MakerDAO’s two tokens and Dai is the most borrowed asset on Compound.[35]

Dharma is a platform for building lending products on Ethereum.[36] Dharma is a platform for building decentralized lending products and facilitates peer-to-peer crypto lending, directly from each user’s personal wallet.[37] One such product is Dharma Lever, which provides instant margin loans for traders using ETH-based assets. This platform facilitates peer-to-peer crypto lending, directly from each user’s personal wallet, by allowing each party of the loan to be discoverable. Borrowers can customize their loan terms including asset type, collateral, and duration. Lenders set a risk profile by specifying their desired loan terms. Borrowers receive principal instantly after they lock up collateral in a smart contract.

The remittance market is similar to the loan market with regards to the potential for disruption by DeFi Dapps. The existing remittances market requires migrant workers who wish to send part of their income across borders to their families in their home countries to pay significant fees. DeFi Dapps often offer the same service for significantly lower fees.

c) Trading

Trading of digital assets is another significant market segment of DeFi Dapps. Several DeFi protocols enable derivatives, margin trading, and prediction markets on Ethereum. Users can trade margins and derivatives,[38] lend margins,[39] and can be issued short or long ERC-20 tokens representing the payouts of the contract, which can be exchanged or posted for sale.[40] Augur operates as a decentralized futures market on Ethereum.[41] Because there is no intermediary, operation costs are reduced, which can maximize the societal benefit-cost ratio of improved forecasts.[42] The decentralized prediction market allows users to bet on, or create a market for, the outcome of any event, ranging from political elections to sports.[43]

1. DeFi Evolution

DeFi products and markets are constantly morphing and will be subject to continuing evolutionary trends as core decentralized infrastructure products become more viable while others devolve.

a) Growth Estimates

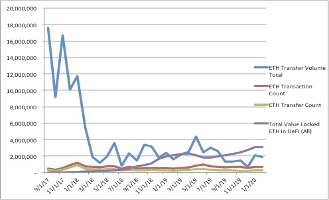

Figures [__] to [__] provide an overview of the evolving DeFi market and its separation from the overall market in Ethereum transactions. Figure [__] highlights the difference between the overall ETH transfer count and the total value locked in ETH of DeFi transactions. Figure [__] suggests that the DeFi marketplace is evolving so far not in terms of growth of the total number of transactions on the Ethereum network but in terms of the total value of the transactions.

Figure [__]: source: glass node and defipulse (ETH Transfer Count — the total amount of transfers. One transaction can trigger one or more transfers. Only successful, non-zero transfers are counted, Source explains TVL (total value locked) is calculated by pulling the balance of ETH and ERC-20 tokens held by each protocol’s underlying smart contracts. The data shown is the data from the 15th of each month, “All” was directly from the website — not generated).

Figure [__] further explains the trend illustrated in Figure [__] above in terms of other transaction measures. Figure [_] illustrates that the value of the ETH transfer volume depreciated from 9/1/17 to 5/1/18 lockstep with the withering away of the ICO market, Bitcoin value and is associated with the emergence of the so-called crypto winter. In its aftermath, finance professionals have started to develop more and more Ethereum based financial products which gave rise to the birth of DeFi and is illustrated by the total value locked of ETH in DeFi (All).

Figure [__]: Source: Glass Node for ETH data and DeFi Pulse (Glass Node — ETH Data, Source defines “Transfer Volume Total” as The total amount of coins transferred on-chain. Only successful transfers are counted, Source defines “Transaction Count” as The total amount of transactions. Only successful transactions are counted, Source defines “Transfer Count” as the total amount of transfers. One transaction can trigger one or more transfers. Only successful, non-zero transfers are counted, DeFi Pulse — TVL, Source explains TVL (total value locked) is calculated by pulling the balance of ETH and ERC-20 tokens held by each protocol’s underlying smart contracts. The data shown is the data from the 15th of each month, “All” was directly from the website — not generated).

Figures [_] to [_] further illustrate the breakdown of the increase in value locked in DeFi transactions as illuminated in Figures [__] and [__] above. In particular, Figure [__] shows that DeFi lending before the breakout of the Covid-19 pandemic generated the majority of value locked in DeFi transactions. Some evidence exists that the market develeveraged most of the lending value as margin calls forced DeFi lenders to deleverage during the pandemic.

Figure [__]: Source: DeFiPulse.com (Source explains TVL (total value locked) is calculated by pulling the balance of ETH and ERC-20 tokens held by each protocol’s underlying smart contracts. The data shown is the data from the 15th of each month.)

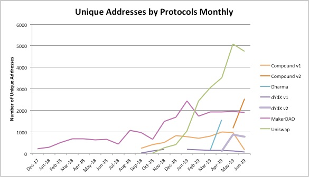

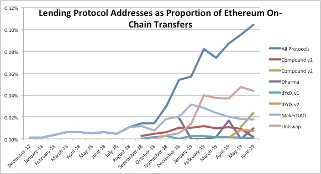

Figures [__] and [__] illustrate which ethereum-based protocols generate a proportion of the overall DeFi transactions.

Figure [__]: Source: Bloxy — Lending Protocols Dynamics Comparison (Source categorized the graphs under Decentralized Protocols analytics, Value Analysis. This category was lending protocols dynamics comparison. Graphs titled “Monthly Cumulative Locked Amount, Unique addresses by Protocol” and “Unique Addresses vs Locked Amount by Protocols Monthly”)

Figure [__] highlights the important role MakerDao, a key stable coin, plays in the DeFi market. The locked dollar amount associated with the unique address for MakerDAO constitutes the overwhelming majority of all unique addresses and associated dollar amount of DeFi transactions.

Figure [__]: Source: Bloxy — Lending Protocols Dynamics Comparison (Source categorized the graphs under Decentralized Protocols analytics, Value Analysis. This category was lending protocols dynamics comparison. Graphs titled “Monthly Cumulative Locked Amount, Unique addresses by Protocol” and “Unique Addresses vs Locked Amount by Protocols Monthly”)

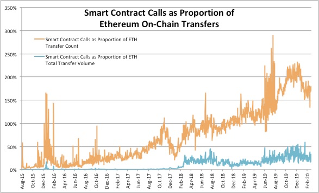

Figure [_] further illustrates the power of DeFi transactions in the Ethereum transaction universe. As Figure [_] shows, smart contract calls constitute a very significant proportion of the ETH transfer count. This appears to be support for the proposition that DeFi financial products built into Ethereum smart contracts play a significant role in the development of the Ethereum network and will likely continue to play that significant role at an increasing scale.

Figure [__]: Source: Bloxy (Proportions obtained by dividing value for monthly smart contract calls by the ETH value, Smart contract call data — Source categorized the graphs under Decentralized Protocols analytics, Value Analysis. This category was Smart Contract Calls, Daily. Graph titled Dynamics of smart contract calls (external only). The data for smart contract calls in the above was generated by taking the monthly sum for contract calls, ETH Transfer Count — the total amount of transfers. One transaction can trigger one or more transfers. Only successful, non-zero transfers are counted, Source defines “Transfer Volume Total” as The total amount of coins transferred on-chain. Only successful transfers are counted).

b) Growth Factors

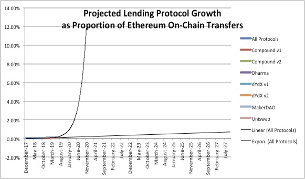

DeFi’s growth rate, illustrated in Figures [___], and expected growth rate, illustrated in Figures [__], provide an early impression of what the digital asset market could morph into. Some of the core features of DeFi provide benefits that have significant comparative advantages over existing legacy finance and FinTech businesses.

Several factors contribute to DeFi’s growth rates and foreshadow the possible evolution of the market for digital assets. At the beginning of the 2020s, DeFi has started to capitalize on its core features to expand into existing legacy businesses. DeFi’s decentralized payment networks facilitate online and offline commerce with low-cost, secure, instant and global payments. Low transaction costs benefit consumers as well as merchants by enabling profit maximization and reducing barriers to entry for new business models, such as micropayments. Several examples illustrate the crossover of DeFi into the more mainstream financial commerce. For example, Square, a centralized payment platform, may incorporate Bitcoin Lightning Network into its payment services.[1] Ripple is at the forefront of decentralized payment networks and has partnered with financial institutions such as MoneyGram to improve the efficiency of cross-border money transfers.[2]

(1) Decentralization

Most of the comparative advantages of DeFi derive from its decentralized features. DeFi is efficient, more decentralized than any other financial solution, and borderless. In theory, because of its higher degree of decentralization in finance, DeFi can protect against monopolization, censorship, mutability, and counterparty risk. The decentralized nature of DeFi transactions makes it less likely that a single node or entity can monopolize the network and exclude others from participating, allowing broad access to the benefits of network effects.[3] It also facilitates easy and instantaneous value transfer without regulatory intermediaries as it is less reliant on a central bank or government.[4]

The decentralized nature of DeFi Dapps via blockchain technology also enables unparalleled transparency. The transparency offered by the technology allows parties in the supply chain real-time access to inventory records and payments can be effected in real-time. The real-time transparency enhancements could facilitate a seamless system of lending and repayment using smart contracts.[5] In turn, DeFi’s transaction transparency has the potential to expand the scope and scale of transactions, protect transacting parties, and facilitate a quick response to financial crises and promote financial inclusion and innovation.

DeFi can promote financial inclusion. Because DeFi transactions are typically open source, fully transparent, and permissionless, anyone with an internet connection can access it. Polycentric governance structures can help achieve communication and consensus between the full set of participants.[6] The underlying programming for DeFi projects is publicly available under a creative commons copyright license and allows nonprofit usage of open source code.[7] Self-custody via encrypted wallets removes costly intermediation that can give the unbanked an opportunity to participate in the value creation. DeFi instruments can help secure and grow the life savings of citizens living in unstable countries, such as Venezuela.[8] In DeFi’s financial alternative, individuals can convert their fiat (government-backed) currency into a stable cryptocurrency (“stablecoin”), store the stablecoin in an interest-bearing account, and use futures contracts to hedge against financial uncertainty. By converting fiat currency into cryptocurrency, migrant workers and refugees can recover their funds even if their property is confiscated while fleeing their home country.

The emerging interoperability of DeFi Dapps further enhances the benefits of DeFi’s decentralization. Interoperability of DeFi transactions could provide further benefits for the evolution of the market in digital assets. At the beginning of the 2020s, DeFi is still largely relegated to the use of one dominant platform. 87% of all publicly funded DeFi projects have been built on Ethereum.[9] Further enhancement of the interoperability of DeFi would increase value flow seamlessly across different services and borders. Interoperability as envisioned by Cosmos and Polkadot,[10] would mean that different blockchains can be interconnected, allowing for enhanced interoperability and increased value flow.

(2) Disintermediation Beyond FinTech

DeFi upgrades financial disintermediation above and beyond FinTech. Financial institutions connect market participants and build trust by serving as an intermediary, thereby reducing transaction costs.[11] Financial technology is increasing efficiency by serving as an intermediary and taking up these roles. Financial technology (FinTech) can further reduce transaction costs by expand transaction scope and empowering peer-to-peer transactions that disintermediate. In existing centralized forms of financial technology disintermediation users are still dealing with a technology company as intermediary instead of a financial institution.[12] Accordingly, centralized financial technology disintermediation is incomplete and allows for further improvements. DeFi attempts to provide such decentralized financial solutions.

DeFi is more efficient than existing financial intermediation, including FinTech. Its superior efficiency can be traced to its extensive reliance on code and automation that remove large parts of the human element and the associated errors and inefficiencies. Entry and exit of network participants are possible at comparatively very low cost which increase efficiency gains.[13] Distributed ledger technology has the potential to allow participants to make joint investments in shared infrastructure without assigning market power to the platform operator, helping increase efficiency of operations.[14]

DeFi can help increase competition and accelerate the pace of financial innovation beyond FinTech. DeFi’s permissionless and open source nature creates an environment that promotes innovation above and beyond FinTech. Decentralized financial applications and platforms publicly share their core technologies through permissive open-source licensing.[15] Since the early days of digital assets, the permissionless open-source environment allowed the developer community to freely build and experiment with new applications.[16] The DeFi framework allows users can combine different protocols to create new financial products and services.[17]

DeFi can scale up savings flows between investors and issuers without having to go through a highly centralized global or national financial ecosystem. DeFi can enable the formation of communities of different types of investors extending beyond geographical boundaries to finance local public goods. These alliances can operate as conduits for financing and feedback between small responsible investors and issuers.[18]

(3) Counterparty Risk Management

DeFi has the potential to address the issue of counterparty risk and associated regulatory concerns. A large part of the regulatory infrastructure that pertains to legacy systems revolves around issues concerning counterparty risk. Yet, the existing regulatory infrastructure is still mostly a patchwork of solutions that has not fully addressed the issue of counterparty risk. DeFi has the potential to address these shortcomings. DeFi reduces counterparty risk because there is no need to trust a third-party intermediary to custody funds or validate transactions.[19] Because DeFi transactions are typically stored and recorded on a public blockchain, DeFi’s transaction transparency can expand the scope and scale of transactions as well as protect transacting parties. Transactions recorded on public ledgers that can be easily viewed and verified,[20] can expand the scale and scope of transactions.[21] Transparency is further enhanced because DeFi is typically built with open source code, the system is auditable by external parties.[22] Finally, counterparty risk that materialized in past financial crises may be addressed by DeFi’s public records of all historical transactions. Financial crises that involve issues of counterparty risk management may be less likely in a DeFi environment.[23]

(4) StableCoins

Since 2019, stablecoins have become a staple in the emerging DeFi market. The total volume of stable cryptocurrencies relative to the rest of the cryptocurrency market is growing consistently.[24] The growth of stable cryptocurrencies can largely be traced back to attempts to combine the utility and benefits of cryptocurrencies and blockchain technology with remedies for the existing fluctuation and volatility in the cryptocurrency markets.[25] The growth data suggests that demand for products that help manage the volatility inherent in other crypto assets is likely to continue to increase.[26]

The emergence of stablecoins in the DeFi infrastructure is accompanied by changes in the legacy banking environment. Cash and bank notes are gradually losing ground to other payment systems.[27] Cash usage in the United States, the United Kingdom, the Netherlands, Sweden, Finland, Canada, France, among other industrialized nations, has fallen well below 50% of total transaction volume.[28] Most significantly, in Northern Europe as few as one in every five transactions is made in cash.[29] The end of technological life cycles of legacy systems and associated emerging trends in payment systems necessitate central banks’ enhanced examination of cryptocurrency solutions.[30]

The renaissance in privately issued stablecoins is, in part, triggered by evolving non-cash alternative needs of existing central banks. Central banks in countries with rapidly declining cash usage[31] are subject to the most pressure to find solutions for bank note alternatives. The cost of cash is also afflicting the existing cash system. In the United States, transacting in cash costs the consumer around 200 billion dollars annually — about $637 per person.[32] The cost of cash is primarily associated with counting, managing, storing, transporting, guarding, and accounting for bank notes.[33] The theft of cash alone costs U.S. retail businesses losses around $40 billion annually.[34] The poor and those with less access to institutions bear a disproportionate share of the costs of using cash.[35]

(5) DAO Prospects

Most of the applications and uses of digital currencies are improved and expanded with well-functioning and well-governed decentralized autonomous organizations (“DAOs”). A DAO is an organization that runs through rules encoded in smart contracts.[36] The first DAO, in May 2016, the crowdfunding campaign, the DAO, operated on Ethereum and set the record for the largest crowdfunding campaign in history with $120 million worth of Ether raised.[37] DAOs help upgrade digital assets across the spectrum of applications and uses. This includes digital assets that can be used as mediums of exchange, speculation,[38] payment rail for non-expensive cross-borders money transfer, and non-monetary uses such as time stamping.[39] Additional use cases of DAOs include financial transactions, secure voting, autonomous organizations, company management, freedom of speech networks, online games, crowdfunding, and speculation.[40]

DAOs are organizations that run through rules encoded in smart contracts.[41] Smart contracts are executed when the conditions embedded in them are recognized as math by the network.[42] Ethereum’s more flexible programming language, Solidity, enables the development of smart contracts[43] in conjunction with Ethereum’s Virtual Machine (EVM), upon which every Ethereum node runs to maintain consensus. EVM is Turing-complete, meaning that it can perform calculations that any other programmable computer is capable of, enabling execution of code exactly as intended.[44] This is the unique feature of the Ethereum network that enables smart contracts and a high level of flexibility in digital innovation, which makes the platform attractive to developers.

Regulatory uncertainty is holding back the development of DAOs and the optimization potential of DAOs for digital assets. The DAO claimed to be a crowdfunding contract and made unregistered offers and sales of DAO tokens in exchange for Ether.[45] However, the SEC began an investigation and determined that, although the DAO claimed to be a crowdfunding contact, it did not meet the SEC’s requirements for a Regulation Crowdfunding exemption because the DAO is neither a broker-dealer nor a funding portal registered with the SEC and the Financial Industry Regulatory Authority.[46] In July 2017, following this investigation, the SEC issued an investigative report stating that virtual coins or tokens may be securities and subject to securities laws, depending on the facts and circumstances including the economic realities of the transaction. The SEC stated that federal securities laws apply to those who offer and sell securities in the United States, regardless of whether the issuing entity is a traditional company or a decentralized autonomous organization, regardless of whether securities are purchased using fiat or virtual currency, regardless of whether they are distributed in certificated form or through distributed Ledger technology. Federal securities laws provide disclosure requirements and regulatory scrutiny aimed at investor protection.[47]

c) Growth Limitations

DeFi is subject to several growth limitations that may undermine its evolution. It is crucial for decentralized finance technologies to be market-driven rather than novelty-driven. Moreover, DeFi technologies need to be both user-friendly and useful for users.

At the beginning of the 2020s, DeFi was not sufficiently user friendly. Anyone who ever interacted with metamask, myetherwallet or scatter, among other core DeFi user interfaces, can attest that dealing with public and private keys requires levels of technical know-how most lay users do not possess. As with most innovative technologies, the digital asset market also resulted from a technology push rather than a market pull.[48] Rather than focusing on usefulness and user-friendliness of new platforms, developers were inspired by technical advancement and started experimenting with new possibilities of the technology to try to discern how to make a profit from their product experimentation.[49] Market pull may evolve if and when the DeFi technology infrastructure is more developed. With a sufficiently developed technology infrastructure it will be possible for the consumer adoption to drive the innovation of new decentralized financial technologies rather than technical novelty.

DeFi platform technologies often have a limited product market fit. The reliance on code in the market for digital assets over human judgments resulted in a focus on products that predominantly rely on automation, ignoring the human element in financial transactions. Because DeFi relies on code rather than human judgment, DeFi products often do not leverage human knowledge and subjective judgment, which limits limiting the potential value of the technology. DeFi technologies are most effective when analyzing inputs that can be objectively recorded and verified and publicly recorded. However, human interaction in business are often too complex to be fully codified objectively. By excluding all non-objective information from the product analysis, all available information may not be fully utilized which limits efficiency and potential usefulness of DeFi.

DeFi lacks a clear regulatory framework which makes its adoption and consumer confidence uncertain. There is insufficient or non-existent regulatory guidance, court decisions, and uncertainty over applicable jurisdiction. Lack of regulatory recognition of blockchain technology is problematic not only for users but for developers. Clear regulatory framework is needed to support reasonable innovation. Courts’ perception and treatment of blockchain technology is uncertain because they have not reviewed, assessed, or scrutinized the uses and applications of blockchain technology. Human intervention is needed to settle legal disputes, even involving smart contract transactions, and is even helpful to create regulatory certainty.[50]

Accountability in DeFi can be a concern. “Without central entity involvement, who should be held accountable for potential wrongdoing can become unclear. Who do you resort to for help? When problems arise, no central party can take actions to freeze transactions, fix problems and restore normal operations.”[51] At the beginning of the 2020s, crypto custody solutions to store cryptocurrencies either lacked transparency, safety, or liquidity.[52]

Finally, DeFi can be vulnerable to fraud and untested financial innovations.[53] Non-existent links to physical/traditional assets.[54] Limited on-chain throughput.[55]

d) DeFi Infrastructure Case Study

In the early 2020s, the DeFi technology infrastructure was insufficiently developed to support DeFi growth estimates and growth potential. To truly fulfill its potential, the DeFi infrastructure development necessitates significant tradeoffs between scaling, security, and levels of decentralization. The trade-off between transaction approval speed and immutability has the potential to undermine the DeFi infrastructure in the long run.[56] Achieving broad consensus among key stakeholders to implement major upgrades is costly and often challenging.[57] All information must be distributed to all parties publicly, then validated through distributed consensus, and stored, a process which requires a great deal of computational power.[58] Creating consensus requires increase costs of prepping, processing, and storing information.[59] On the other hand, fewer computational checks for consensus increase the risk of collusion attacks that could change the record.[60] The flipside of the transparency offered by DeFi is the competing interest of user privacy, plus associated processing costs to achieve privacy.[61]

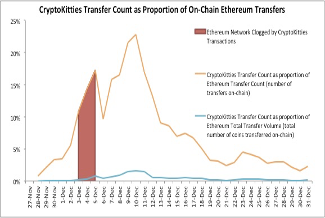

A specific example that may raise concerns with regard to the DeFi infrastructure development is the case of cryptokitties. Cryptokitties is a game of digital collectibles on the Ethereum blockchain.[62] In one of the earliest attempts to apply blockchain technology to gaming, cryptokitties allows players to breed, purchase, and sell virtual cats of different origin. Significantly, cryptokitties is one of the first instantiations of true digital assets that create an inherent value for its users. In December 2017, the game’s popularity slowed down the Ethereum network by causing an all-time high in number of transactions.[63]

Figure [__] illustrates that in early December 2017 the Ethereum network experienced significant delays in transaction processing which was in part caused by the Cryptokitties DApp.

Figure [__]: Source: GlassNode, Bloxy.info (Proportions obtained by dividing value for CK transfer by the ETH value, CK transfer — Source titles this data “CK Transfer Count” with no further explanations, ETH Transfer Count — the total amount of transfers. One transaction can trigger one or more transfers. Only successful, non-zero transfers are counted, Source defines “Transfer Volume Total” as The total amount of coins transferred on-chain. Only successful transfers are counted) Source: Bloxy.info — CryptoKitties Population, Articles on network crash caused by Cryptokitties — came out 11/28/2017, by 12/4 (date of QZ article), SOURCE 1: BBC (published 12/5/17) https://www.bbc.com/news/technology-42237162,[64] SOURCE 2: QZ.COM (published 12/4/17) https://qz.com/1145833/cryptokitties-is-causing-ethereum-network-congestion/[66], SOURCE 3: COINMETRICS’ STATE OF THE NETWORK (Published 11/2019) https://coinmetrics.substack.com/p/coin-metrics-state-of-the-network-b34.[67]

A comparison of ETH transfer count and cryptokitties transfer counts in Figures [__] amd [__] suggests that the cryptokitties effect on the Ethereum network could have larger implications if the Ethereum network and expected transaction volume continue to grow.

Figure [__]: Source: GlassNode, Bloxy.info (CK transfer — Source titles this data “CK Transfer Count” with no further explanation, ETH Transfer Count — the total amount of transfers. One transaction can trigger one or more transfers. Only successful, non-zero transfers are counted)

In light of the network capacity issues illustrated by the cryptokitties shutdown in Figures [__] and [__], the expected growth rate illustrated in Figures [__] and [__] could mean that the Ethereum network will continue to experience network shortages and throughput issues unless the Ethereum infrastructure is upgraded to deal with the expected volume of transactions. Of course, correlation is not causation and many other factors could call the DeFi technology infrastructure into question.

Figure [__]: Source: Bloxy — Lending Protocols Dynamics Comparison; GlassNode, Proportion obtained by dividing address number by ETH transfer count. Lending protocol dynamics from the circle data above — This data was the circle graphs we looked at on Wednesday that you requested. It is near the bottom of the link. Source categorized the graphs under Decentralized Protocols analytics, Value Analysis. This category was lending protocols dynamics comparison. Graphs titled “Monthly Cumulative Locked Amount, Unique addresses by Protocol” and “Unique Addresses vs Locked Amount by Protocols Monthly, ETH Transfer Count — the total amount of transfers. One transaction can trigger one or more transfers. Only successful, non-zero transfers are counted.)

Figure [__]: Source: Bloxy — Lending Protocols Dynamics Comparison; (GlassNode, Same graph as immediately above, adding in projections using linear and exponential growth models for the “all protocols as proportion of ETH on-chain transfers” data.)

[1] Leigh Cuen, Square CEO Jack Dorsey Says Bitcoin’s Lightning is Coming to Cash App., CoinDesk (Feb. 11, 2019), https://www.coindesk.com/square-bitcoin-jack-dorsey-lightning-cash-app).

[2] Ripple Announces Strategic Partnership With Money Transfer Giant, MoneyGram, Ripple: Insights (Jun. 17, 2019), https://ripple.com/insights/rippleannounces-

strategic-partnership-with-money-transfer-giant-moneygram.

[3] Gur Huberman, Jacob D. Leshno and Ciamac Moallemi, An Economist’s Perspective on the Bitcoin Payment System, 109 AEA Papers and Proceedings 93 (2019), https://www.aeaweb.org/articles?id=10.1257/pandp.20191019.

[4] Saifedean Ammous, The Bitcoin Standard: The Decentralized Alternative to Central Banking (2018).

[5] Wang, et al., supra noate 82; Lee, supra note 82.

[6] Bose, et al., supra note 79 at 287.

[7] Shaughnessy, Demarco & Lulla, supra note 73 at 3.

[8] Leonhard, supra note 45 at 4.

[9] Chen and Bellavitis, supra note 83 at 3.

[10] Polkadot https://polkadot.network/, and Cosmos https://cosmos.network/

[11] Chen and Bellavitis, supra note 83 at 1.

[12] Id.

[13] Bose, et al., supra note 79.

[14] Christian Catalini & Joshua S. Gans, Some Simple Economics of the Blockchain, Nat’l Bureau of Econ. Res. Working Paper №22952, (Dec. 2016 revised Jun. 2019).

[15] Chen and Bellavitis, supra note 83 at 2–3. See also Shaughnessy, Demarco & Lulla, supra note 73 at 3.

[16] Henry Chesbrough and Marshall Van Alstyne, Permissionless Innovation, 58 Communications of the ACM 24 (2015); Vint Cerf, Remarks at the Digital Broadband Migration: The Dynamics of Disruptive Innovation, 10 J. Telecomm. High Tech. L. 21 (2012).

[17] Erik Bynjolfsson and Andrew McAffee, The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies (2014).

[18] See Bose, Dong, & Simpson, supra note 79 at 283.

[19] Shaughnessy, Demarco & Lulla. supra note 73 at 3.

[20] Chen and Bellavitis, supra note 83 at 3–4.

[21] Marc-David L. Seidel, Questioning Centralized Organizations in a Time of Distributed Trust, 27 J. of Mgmt. Inquiry 40 (2018).

[22] Shaughnessy, Demarco & Lulla, supra note 73 at 3.

[23] Andrew W. Lo, Reading About the Financial Crisis: A Twenty-One-Book Review, 50 J. of Econ. Literature 151, 174 (2012).

[24] Compare the google search results for “blockchain” were exceeded by “stablecoin” in the mid 2019s. https://consensys.net/blog/news/2019-was-the-year-of-defi-and-why-2020-will-be-too/

[25] Stablecoin, Binance Academy, https://www.binance.vision/glossary/stablecoin (last visited Apr. 24, 2019).

[26] Can JPM Coin Disrupt the Existing Stablecoin Market?, Binance Research (Mar. 1, 2019) at 4, https://info.binance.com/en/research/marketresearch/img/BinanceResearch-JPMCoin.pdf.

[27] Kenneth S. Rogoff, The Curse of Cash (2016); Jonathan Brugge et al., Attacking the Cost of Cash, McKinsey & Company (Aug. 2018), https://www.mckinsey.com/industries/financial-services/our-insights/attacking-the-cost-of-cash.

[28] “Germany, Japan, and Austria stand apart as wealthy countries where consumers maintain a strong preference for cash at the point of sale, despite universal availability of electronic payments instruments and the broad adoption of electronic transfers for recurring payments.” Id.

[29] Id.

[30] Bech & Garratt, supra note 35.

[31] Brugge et al., supra note 301.

[32] Brugge et al., supra note 301.

[33] Aleksander Berentsen & Fabian Schar, The Case for Central Bank Electronic Money and the Non-case for Central Bank Cryptocurrencies, 100 Fed. Res. Bank St. Louis Rev. 97 (2018).

[34] Will Yaowicz, Cash Costs U.S. Businesses $40 Billion a Year, Inc.com, https://www.inc.com/will-yakowicz/dealing-with-cash-costs-american-businesses-55-billion.html (last visited Apr. 24, 2019).

[35] Id.

[36] DAO, Crypto Glossary, Coinmarketcap.com, https://coinmarketcap.com/glossary/ (last accessed April 8, 2020).

[37] Charfeddine, supra note 13 at 209.

[38] A. Rogojanu & Liana Badea, The Issue of Competing Currencies: Case Study — Bitcoin, 21 Theoretical Applied Econ. 103 (2014); Paola Ceruleo, Bitcoin: a rival to fiat money or a speculative financial asset? (2014) (on file with Luiss Guido Carli).

[39] Robleh Ali, et al. The Economics of Digital Currencies, Bank of England: Q. Bull. 276 (2014).

[40] Besarabov, supra note 13 at 1.

[41] Crypto Glossary, supra, note 7.

[42] Charfeddine, et al., supra note 6 at 201.

[43] Crypto Glossary, supra, note 310.

[44] Ethereum’s Virtual Machine, Crypto Glossary, Coinmarketcap.com, https://coinmarketcap.com/glossary/ (last accessed April 8, 2020).

[45] SEC Issues Investigative Report Concluding DAO Tokens, A Digital Asset, Were Securities U.S. Securities and Exchange Commission (Jul. 25, 2017) (citing to, Report f Investigation Pursuant to Section 21(a) of the Securities Exchange Act of 1934: The DAO, U.S. Securities and Exchange Commission (Jul. 25, 2017)).

[46] SEC, https://www.banking.senate.gov/imo/media/doc/Clayton%20Testimony%202-6-18.pdf

[47] Id.

[48] Richard Partington, How the Wheels Came Off Facebook’s Libra Project, Guardian (Oct. 18, 2019, 9:42 AM), https://www.theguardian.com/technology/2019/oct/18/how-the-wheels-came-off-facebook-libra-project.

[49] Id.

[50] See Reggie O’Shields, Smart Contracts: Legal Agreements for the Blockchain, 21 N.C. Banking Inst. 177 (2017), http://scholarship.law.unc.edu/ncbi/vol21/iss1/11.

[51] Robert Palatnick, Governing DLT Networks: Distributed Ledger Technology Governance for Private Permissioned Networks (Sept. 2019), https://perspectives.dtcc.com/articles/governing-dlt-networks.

[52] CDx, https://cdxproject.com/. See also Young, A. and Wilson, J., CDx: Credit Default Swaps on the Ethereum Public Blockchain, Sep. 4, 2018, https://cdxproject.com/assets/resources/cdx-whitepaper.pdf, at 1.

[53] Chen and Bellavitis, supra note 83 at 6.

[54] Shaughnessy, Demarco & Lulla, supra note 73 at 3.

[55] Shaughnessy, Demarco & Lulla, supra note 73 at 3.

[56] Bose, Dong, & Simpson, supra note 79 at 304

[57] Akhil Kumar, Rong Liu, & Zhe Shan, Is Blockchain a Silver Bullet for Supply Chain Management? Technical Challenges and Research Opportunities, 51 Decision Sci. 9 (2019).

[58] Eric Budish, The Economic Limits of Bitcoin and the Blockchain, National Bureau of Economic Research Working Paper №24717 (2018) (on file with publisher).

[59] Kumar, Liu, & Shan, supra note 330.

[60] Bose, Dong, & Simpson, supra note 79 at 304

[61] Chen and Bellavitis, supra note 83 at 6.

[62] CryptoKitties, Wikipedia, https://en.wikipedia.org/wiki/CryptoKitties (last visited May 20, 2020).

[63] CryptoKitties Craze Slows Down Transactions on Ethereum, BBC: Technology (Dec. 5, 2017), https://www.bbc.com/news/technology-42237162.

[64] Why does it matter if CryptoKitties is slowing down Ethereum? According to ETH Gas Station, the CryptoKitties game accounts for over 10% of network traffic on Ethereum. As traffic increases, transactions become more expensive to execute quickly. “The real big issue is other major players looking for alternatives to Ethereum and moving to different systems,” Mr Hileman said. “There’s definitely an urgency for Ethereum to try and address this issue.”

[65] Unprocessed ethereum transactions have risen about six-fold since CryptoKitties was released on Nov. 28, according to data provider Etherscan. CryptoKitties now has the busiest address on the ethereum network, accounting for nearly 12% of all transactions. That’s a threefold increase from Saturday (Dec. 2) when it was responsible for about 4% of all ethereum transactions. The network congestion forced the game’s developers, a Vancouver company called Axiom Zen, to raise prices. This made processing the game’s transactions more attractive to ethereum miners, improving the odds of the transactions being accepted. Some $2.7 million has changed hands on the CryptoKitties marketplace in the six days it has been active, according to data from Crypto Kitty Sales. The developers of the game told Quartz it had 1,165 players on Dec. 1 (Update: the game has 6,600 active players as of Dec. 4, according to Benny Giang of Axiom Zen). 12/3 — Due to network congestion, we are increasing the birthing fee from 0.001 ETH to 0.002 ETH. This will ensure your kittens are born on time! The extra is needed to incentivize miners to add birthing txs to the chain.

[66] Unprocessed ethereum transactions have risen about six-fold since CryptoKitties was released on Nov. 28, according to data provider Etherscan. CryptoKitties now has the busiest address on the ethereum network, accounting for nearly 12% of all transactions. That’s a threefold increase from Saturday (Dec. 2) when it was responsible for about 4% of all ethereum transactions. The network congestion forced the game’s developers, a Vancouver company called Axiom Zen, to raise prices. This made processing the game’s transactions more attractive to ethereum miners, improving the odds of the transactions being accepted. Some $2.7 million has changed hands on the CryptoKitties marketplace in the six days it has been active, according to data from Crypto Kitty Sales. The developers of the game told Quartz it had 1,165 players on Dec. 1 (Update: the game has 6,600 active players as of Dec. 4, according to Benny Giang of Axiom Zen). 12/3 — Due to network congestion, we are increasing the birthing fee from 0.001 ETH to 0.002 ETH. This will ensure your kittens are born on time! The extra is needed to incentivize miners to add birthing txs to the chain.

[67] In late 2017, CryptoKitties burst onto the scene causing ERC-721 (non-fungible token) transactions to reach over 80,000 per day. But after a brief frenzy, CryptoKitty trading died off, and ERC-721 transactions have not topped over 25,000 per day since. CryptoKitties notoriously caused blockchain congestion, and caused ETH fees to spike.

[1] WTF, Story of DeFi: How it Started, Where It Stands Now, DeFi Definition Revisited, Medium: WTF-Dao (Oct. 23, 2019), https://medium.com/wtf-dao/story-of-defi-how-it-started-where-it-stands-now-defi-definition-revisited-628fc3bab308, The name “DeFi”, short for decentralized finance, has similarities with the ideas of “defy”ing something and is, by itself, a reference to a challenge to the existing financial system.

[2] WTF, supra note 67.

[3] Id.

[4] Product Protocol, The History of DeFi, Medium (Dec. 11, 2019), https://medium.com/@product.protocol/the-history-of-defi-f6e11a3c2d6e

[5] Id.

[6] Decentralized financial technologies: report on financial stability, regulatory and governance implications, Financial Stability Board (Jun. 6 2019), https://www.fsb.org/2019/06/decentralised-financial-technologies-report-on-financial-stability-regulatory-and-governance-implications/.

[7] see generally Tom Shaughnessy, Medio Demarco & Anil Lulla, Decentralized Finance (DeFi) Thematic Insights, Delphi Digital (Mar. 2019), https://www.delphidigital.io/defi.

[8] Fenwick, Mark and Kaal, Wulf A. and Vermeulen, Erik P.M., Legal Education in the Blockchain Revolution (March 22, 2017). U of St. Thomas (Minnesota) Legal Studies Research Paper №17–05. Available at SSRN: https://ssrn.com/abstract=2939127

at 6.

[9] Shaughnessy, Demarco & Lulla, supra note 73 at 3.

[10] Arvind Narayanan et al., Bitcoin and Cryptocurrency Technologies: A Comprehensive Introduction (2016).

[11] Lin William Cong and Zhiguo He, Blockchain Disruption and Smart Contracts, 32 Rev. of Fin. Stud., 1754 (2019).

[12] Financial Stability Board, supra note 72.

[13] Satyajit Bose, Guo Dong, & Anne Simpson, The Financial Ecosystem 304 (2019).

[14] Id. at 305.

[15] See Leonhard, supra note 45.

[16] Peter Lee, Trade Finance on Blockchain Moves to Full Commercial Production, 49 Euromoney 590 (2018); Rui Wang, Zhangxi Lin, & Hang Luo, Blockchain, Bank Credit and SME Financing, Quality & Quantity (2019).

[17] Yan Chen and Cristiano Bellavitis, Blockchain Disruption and Decentralized Finance: The Rise of Decentralized Business Models, 13 J. Bus. Venturing Insights 1, 6 (2020).

[18] E.g. Bancor https://www.bancor.network/

[19] E.g. Uniswap Protocol (@UniswapProtocol), Twitter (Feb. 5, 2019, 10:26 AM), https://twitter.com/UniswapExchange/status/1092821767134035968.

[20] E.g., Ren, https://renproject.io/

[21] Shaughnessy, Demarco & Lulla, supra note 73 at 5.

[22] E.g. 0x, https://0x.org/

[23] Shaughnessy, Demarco & Lulla, supra note 73 at 4.

[24] Maker DAO: https://makerdao.com/en/

[25] cite specific number to defipulse https://defipulse.com/

[26] Dai in Numbers: Momentum Report Q3, Maker: Blog (Oct. 8, 2019), https://blog.makerdao.com/dai-in-numbers-momentum-report-q3/.

[27] Compound protocol “about” https://compound.finance/about

[28] Maker, supra note 92.

[29] Compound release, https://compound.finance/about

[30] See Robert Leshner, Compound v2 is Live, Medium: Compound (May 23, 2019), https://medium.com/compound-finance/compound-v2-is-live-157db0b7cfc8.

[31] Robert Leshner, Our Plan to Create Compound v2, Medium: Compound (Mar. 18, 2019), https://medium.com/compound-finance/compound-v2-fe4b1fb62abb.

[32] Leshner, supra note 96; Id.

[33] Zerion, https://zerion.io/ (last visited May 14, 2020).

[34] Opyn, https://opyn.co/#/ (last visited May 14, 2020).

[35] Leshner, supra note 96.

[36] Dr. Sam Scarpino, Dharma Platform: Your Impact-First Technology Partner, Dharma Platform (Jan. 2019), https://dharmaplatform.com/wp-content/uploads/2019/01/Dharma-Platform_Your-Impact-First-Data-Management-Partner-1.pdf.

[37] Dharma Platform, https://dharmaplatform.com/ (last visited May 14, 2020).

[38] dYdX protocol, https://dydx.exchange/

[39] bZx protocol, https://bzx.network/

[40] Daxia protocol, https://www.daxia.us/

[41] Augur, https://www.augur.net/

[42] Jack Peterson, Joseph Krug, Micah Zoltu, Austin K. Williams, & Stephanie Alexander, Augur: A Decentralized Oracle and Prediction Market Platform (Feb. 3 2018) (unpublished manuscript) (on file with Cornell University), https://arxiv.org/abs/1501.01042.

[43] Shaughnessy, Demarco & Lulla, supra note 73 at 14.